A blog database about many distinct and varied topics. Topics include news, science, technology, current events, politics, and more. Use the search bar to find a topic that interests you.

Insights Search

Loading index...

Thursday, July 11, 2019

Forget G-20 News, The Global Manufacturing Recession Is Here

The fundamental problem is that we now need to economically expand the spending power of the whole SE Asian region in particular. Fortunately it is happening and this will slowly absorb all that capacity.

The apparent slow down in China will now force China to resolve a host of internal contradictions which will generate a sound Chinese economy that will likely not include the CCP which is parasitic on the Chinese economy and has been attempting to become equally parasitic on the global economy.

Yet its example now empowers the rest of the world. Thus it is timely that China now consolidates its modernism while everyone else gets their national acts together to also achieve modernism. This process will take a full thirty years.

The temptation to trigger a global world war which will merely destroy wealth briefly needs to be prevented. This must focus on the creation of nation state cities whose purpose is to capture human sentiments and the resolution of global poverty utilizing the power of the rule of twelve.

.

.

Forget G-20 News, The Global Manufacturing Recession Is Here

Wed, 07/03/2019 - 05:00

Authored by Daniel Lacalle, https://www.zerohedge.com/news/2019-07-02/forget-g-20-global-manufacturing-recession-here

The G20 summit has not generated unexpected or

significant headlines and, of course, is not a catalyst for a relevant

change in the global economic trends. The United States and China have only agreed to postpone tariff increases, but no real trade agreement has been reached.

If we look at the last G20 meeting conclusions, nothing has really improved.

Plans to introduce new tariffs are delayed, and the result is exactly

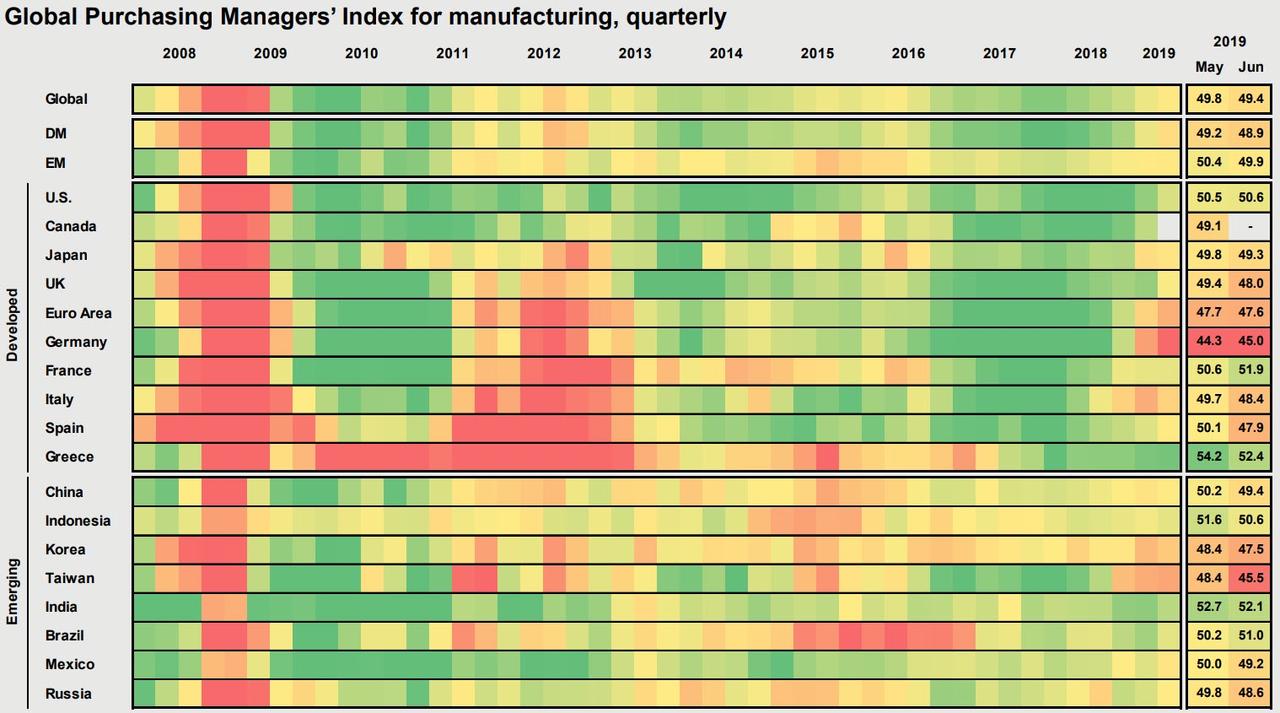

what happened in the previous G20. The real news is the evidence of a

manufacturing recession.

Xi Warns of 'Bullying Practices' Ahead of G-20 Meeting With Trump

Markets have reacted strongly in a relief rally because the trade

dispute did not get worse. The safest assets, such as gold, fell while

the stock markets rose despite a widespread disappointment in

manufacturing PMIs. And therein lies the danger. Many investors are betting again on monetary policy as the only factor to drive markets and risky asset valuations higher.

It is difficult to think that the agreement in the G20 will improve the global economic outlook, mainly

because the weakness of the Eurozone or China and the slowdown of the

manufacturing sector have nothing to do with the so-called trade war,

but with almost a decade of excess in demand-side policies, which have

perpetuated overcapacity, increased debt and made economies less dynamic

by zombifying the low productivity sectors through low rates and

constant refinancing of non-performing debt. If there is any positive news for world economic growth, it

has not come from the G20, but from the agreement between Mercosur and

the European Union, after twenty years of negotiations. The

European Union liberalizes its agricultural, industrial and service

imports and supports an improvement that can be significant for the

economic growth of the countries integrated in Mercosur, as well as

helping the EU revive its stagnant economy. Or at least try.

Unfortunately, these agreements do not reduce the risk of high

indebtedness or excess capacity. The great problem of multilateral

agreements is that they often disguise the errors of debt saturation and

political spending and sometimes increase those mistakes. We are living a kind of “Groundhog Day”, the constant

repetition of something we have already lived: a few smiles, a

handshake, a couple of tweets, reasonably broad and vague messages, but

little in terms of concrete measures. Our estimates of economic growth and corporate profits have not

improved after the G20, and it is worth warning of the risk of

complacency when macroeconomic indicators worsen and investors increase

exposure to risk. What emerges in many cases of this different trend

between macro indicators and market valuations is that there is only one

synchronized bet: More central bank injections. Investors hoping that

data will continue to worsen so that central banks will inject more

liquidity and lower interest rates. At the very least we should be cautious in pro-cyclical

exposure. Macroeconomic data show the evidence of the slowdown and risk

of stagnation. After more than 20 trillion dollars of stimulus, massive deficit

spending and large incentives to increase capex and debt, manufacturing

ind¡ices are in contraction. Businesses have plenty of available capital

at low cost, but face the prospect of weakening demand and

zombification, so manufacturing is showing one of the worst side effects

of cheap money: stagnation from debt saturation and widespread excess

capacity. No trade war truce or central bank quantitative

easing is going to change this trend because central planning and

demand-side policies are the culprits of stagnation, not the solution.

No comments:

Post a Comment