TERRAFORMING TERRA

We discuss and comment on the role agriculture will play in the containment of the CO2 problem and address protocols for terraforming the planet Earth.

A model farm template is imagined as the central methodology. A broad range of timely science news and other topics of interest are commented on.

Search This Blog

Friday, May 3, 2019

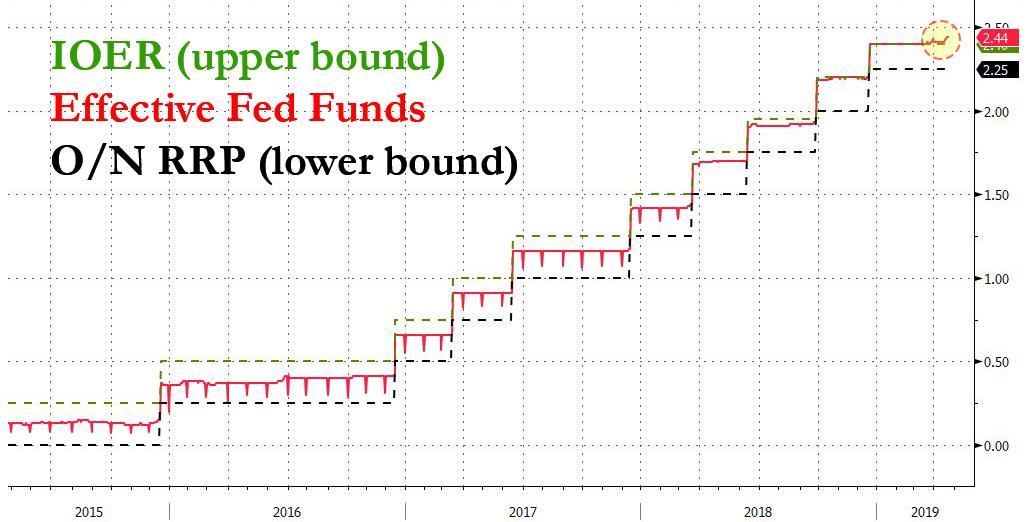

Fed Loses Control Of Rates: Fed Funds Above IOER For Past Month

I do not expect you to make much of this as it in the realm of fine detail in which a temporary adjustment shifts the scales Thus the attempt to explain through tax flows.

Recall though that we have had a sustained lift of interest rates since 2016 back to levels supportive of sound money. At the same time we have seen a full reactivation of the USA labor pool and that is reshaping the landscape of both private and public finance. We are all now on a sound financial basis and everything should steadily improve.

What the infrastructure bill will do is allow a massive credit expansion to consolidate all those gains. With the crap literally about to hit the fan in terms of DEEP STATE criminality, we may get this passed during the next few months or even quicker.

I would like to see it followed by a similar sized move to eliminate poverty as well in such a way that the economy is finally optimized and actually able to attain eight percent in annual growth..

Fed Loses Control Of Rates: Fed Funds Above IOER For Past Month

Something

unexpected has been going on in overnight funding markets: ever since

March 20, the Effective Fed Funds rate has been trading above the IOER. This is not supposed to happen.

As a reminder, ever since the financial crisis, in order to push the

effective fed funds rate above zero at a time of trillions in excess

reserves, the Fed was compelled to create a corridor system for the fed

funds rate which was bound on the bottom and top by two specific rates

controlled by the Federal Reserve: the "floor" for the corridor was the

overnight reverse repurchase rate (ON-RRP) which usually coincides with

the lower bound of the fed funds rate, while on top, the effective fed

funds rate is bound by the rate the Fed pays on Excess Reserves (IOER),

which served as the corridor "ceiling."

Or at least that's the theory. In practice, the effective FF tends to

occasionally diverge from this corridor, and when it does, it prompts

fears that the Fed is losing control over the most important instrument

available to it: the price of money, which is set via the fed funds

rate.

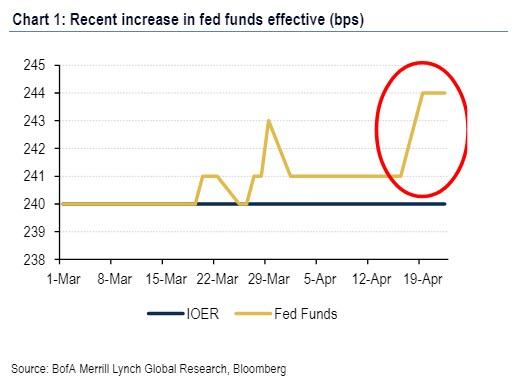

Ever since March 20, this fear is front and center because as shown in the chart below, starting

on March 20, the effective Fed Funds rate rose above the IOER first by

just 1 basis point, and then, last Friday spiked as much as 4 bps above

IOER.

Here is the recent action zoomed in:

Again: this should not be happening and has prompted numerous

concerns among the analyst community what is going on and why has the

Fed - which previously adjusted the IOER specifically to avoid having

the EFF trade outside the corridor - lost control of rates so badly.

In its attempt to explain what is going on, BofA rates analyst Mark Cabana wrote overnight that the spike in the fed funds rate is due to to MMF outflows around the April tax date and elevated GC repo rates. That said, Cabana notes that he has "been surprised by the moves and had expected supply cuts to push FF & repo lower."

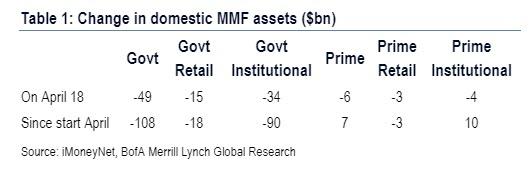

Addressing the first point, BofA notes that the higher money market

rates "have been driven by sizeable MMF outflows, especially from

government funds" as shown in the table below.

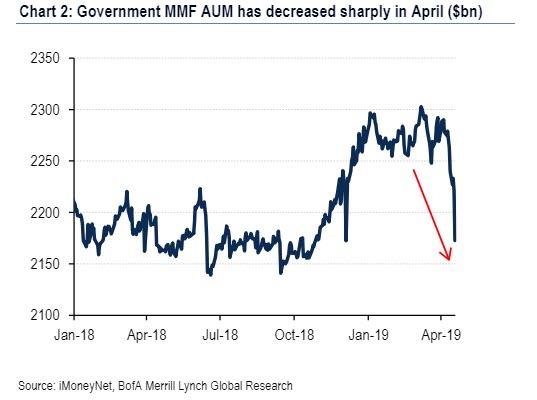

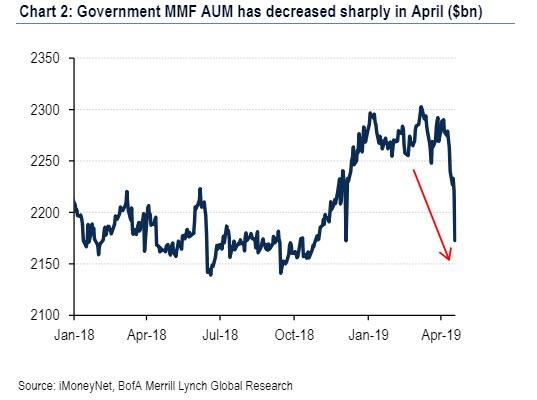

3 While it has not gotten much attention in fund flow circles, the

chart below shows that the AUM of government money-market funds has

declined $108 billion since the start of April with a sizeable $49

billion outflow between Wednesday and Thursday last week according to

iMoneyNet.

According to BofA, these outflows "are mostly tax related as

investors either pulled funds to meet tax liabilities or to replenish

bank deposits from which tax payments were withdrawn." Furthermore,

these MMF outflows have more than offset the $86bn in bill supply cuts

since the start of April and according to Cabana, have likely been the

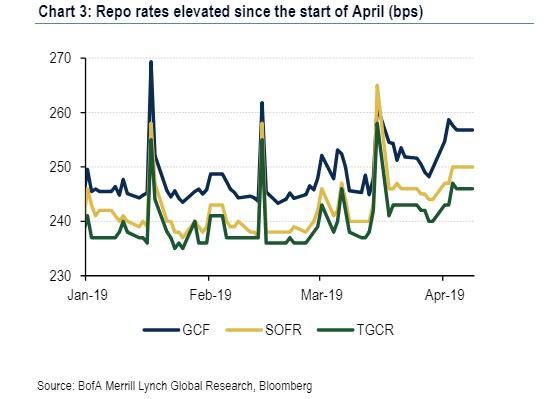

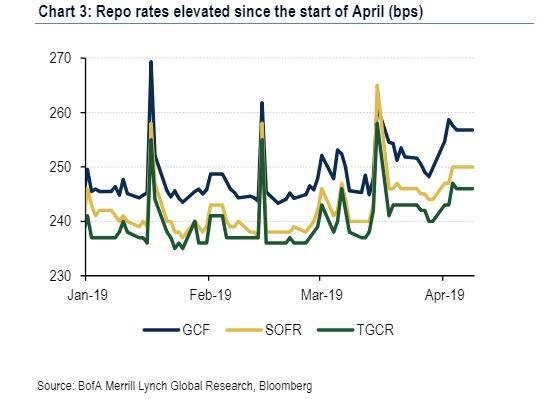

dominant driver contributing to elevated GC repo rates. Indeed, GCF,

SOFR, and TGCR spreads to IOER have all averaged 2.5 to 4.5 bps higher

in April vs similar periods in Q1.

To Bank of America it was these factors plus the shrunk volumes

surrounding Easter holiday trading that led to both lower FF volumes and

higher FF prints.

Here Barclays offers a slightly different explanation.

The bank's rate expert Joseph Abate suggesting that the 3bp rise in fed funds since April 16 "suggests

that moments of upward pressure on the rate will become more frequent

as bank reserves drop, and changes in the level of reserves now have

larger effects on the Fed’s policy target."

Similar to BofA, Barclays believes that a key culprit behind the move

higher in the interest rate are recent tax flows, whereby the

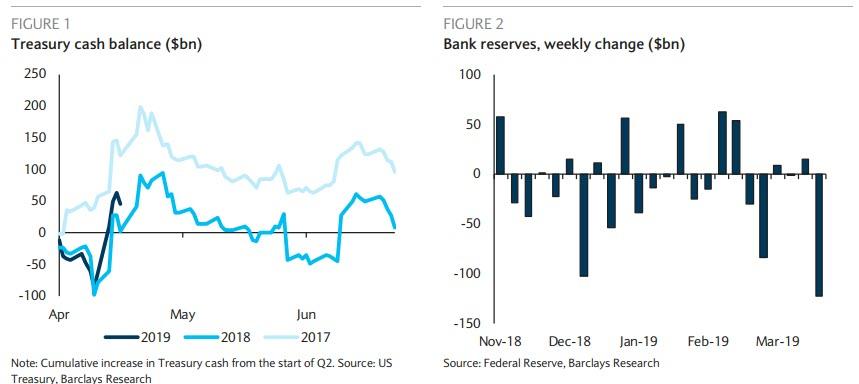

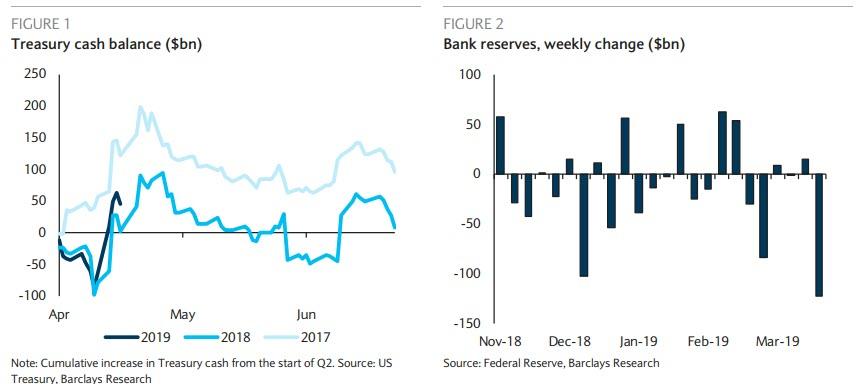

Treasury’s tax collections flow directly into its account at the Fed, and as they are deducted from taxpayers’ bank accounts, they drain reserves. To

demonstrate this point, the bank points out that last week, the

Treasury’s cash balance rose by $124 billion while bank reserves fell by

about $122 billion.

To Abate, who believes the recent spike in FF is temporary although it

may take several days before it normalizes back down to 2.40%/2.41%,

there’s also a risk that there may only be a "partial correction" in the

fed funds rate given that the market is “extremely lopsided,” since the

Federal Home Loan Banks (FHLBs) are the only lender.

More concerning is Abate's conclusion that the large move also

suggests that the banking sector is "nearing the steeply sloping part of

the reserve demand curve" which means that "bank reserves are

now significantly closer to what individual banks consider their ‘least

comfortable level of reserves’ and thus banks are more willing to pay

higher rates to retain these balances."

In other words, some $1.5 trillion in excess liquidity created by the

Fed is no longer enough for banks which are starting to scramble to

obtain additional liquidity, which needless to say, is very troubling

for a banking system which is supposedly "fortress" and "much more

stable" than it was before the financial crisis. If anything, this means

that even a modest liquidity draining crisis at any point in the future

could have vastly more dire consequences than even the pessimists

believe.

So what should the Fed do to regain control over interest rates?

According to Barclays to address the expected increase in fed funds volatility, the

Fed could either end the balance sheet runoff this summer instead of

waiting until September, create a standing repo facility -

something which has been rumored for months - or conduct standard open

market operations, injecting even more liquidity into the system.

Meanwhile, BofA points out that the recent FF rise has increased speculation the Fed might consider an imminent IOER reduction, possibly at the May meeting next week, even though the bank believes that this is premature for now, and it would likely take FF increasing to and remaining at 2.45% before the Fed seriously considers such a move. Additionally,

the Fed would likely also want to give the market advance notices as it

has in the past preferred to signal such a move in advance via the

minutes. Here it is worth noting that the Nov minutes indicated the Fed

might consider an inter-meeting technical IOER adjustment if needed.

This suggests the Fed could act quickly to adjust IOER lower but clearer

signals of FF at or above 2.45% would be needed to justify such a move.

In other words, the Fed won't rush to "regain" control of interest

rates until it becomes patently obvious to everyone that it has lost

control.

No comments:

Post a Comment