Faking a gold bar using tungsten actually works well. Same weight. Not so using copper. I am cautious thinking ultrasound would pick up a tungsten fake. This will be particularly true if the gold thickness is really thin which with the smaller bars would be practical. The picture shows us an likely example.

Copper should fool no one at all. There is a real weight difference..

Here it appears that no one went to the expense of making it actually difficult and merely made sure no one asked questions. Thus all the gold used as collateral in China could be fabricated and the real gold has been sent offshore instead.

This is now going to get ugly and i do think that every gold bar in existence should be remelted. It can even be cast into huge gold Buddhas for public display. That woukd at least make this impossible.

Copper should fool no one at all. There is a real weight difference..

Here it appears that no one went to the expense of making it actually difficult and merely made sure no one asked questions. Thus all the gold used as collateral in China could be fabricated and the real gold has been sent offshore instead.

This is now going to get ugly and i do think that every gold bar in existence should be remelted. It can even be cast into huge gold Buddhas for public display. That woukd at least make this impossible.

83 Tons Of Fake Gold Bars: Gold Market Rocked By Massive China Counterfeiting Scandal

by Tyler Durden

Mon, 06/29/2020 - 12:15

Over the years, we have periodically reported of the occasional gold bar discovered as counterfeit in Manhattan's Diamond District which instead of containing the yellow precious metal would be filled with gold-plated tungsten or in some cases copper. The news would spark a brief wave of outrage, prompting physical gold holders to run ultrasound spot checks of their inventory, at which point interest would wane and why not: buyer, after all, beware in gold as in every other market, and if someone is spending thousands to buy fake gold, well that's Darwinism in action.

Yet one market which seemed stubbornly immune to any counterfeiting was that of physical gold in China, which was odd considering that over the past decade China had emerged as the world's biggest counterfeiter of various, mostly industrial metals used to secure bank loans, better known as "ghost collateral", and which adding insult to injury, would frequently be rehypothecated meaning often several banks would have claims to the same (fake) asset.

All that is about to change with the discovery of what may be one of the biggest gold counterfeiting scandal in recent history. And yes, not only does it involve China, but it emerges from a city that has become synonymous for all that is scandalous about China: Wuhan itself.

With that preamble in mind, we introduce readers to Wuhan Kingold Jewelry Inc., a company which as the name implies was founded and operates out of Wuhan, and which describes itself on its website as "A Company with a Golden future."

In retrospect, it probably meant "copper" future, because as a remarkable expose by Caixin has found, more than a dozen Chinese financial institutions, mainly trust companies (i.e., shadow banks) loaned 20 billion yuan ($2.8 billion) over the past five years to Wuhan Kingold Jewelry with pure gold as collateral and insurance policies to cover any losses. There was just one problem: the "gold" turned out to be gold-plated copper.

Some more background: Kingold - whose name was probably stolen from Kinross Gold, one of the world's largest gold miners - is the largest privately owned gold processor in central China’s Hubei province. Its shares are listed on the Nasdaq stock exchange in New York (although its current market cap of just $10MM is a far cry from its all time highs hit when the company IPOed on the Nasdaq around 2010) . The company is led by Chairman Jia Zhihong, an intimidating ex-military man who is the controlling shareholder.

What could go wrong?

Well, apparently everything as at least some of 83 tons of gold bars used as loan collateral turned out to be nothing but gilded copper. That has left lenders holding the bag for the remaining 16 billion yuan of loans outstanding against the bogus bars. And as Caixin adds, the loans were covered by 30 billion yuan of property insurance policies issued by state insurer PICC Property and Casualty and various other smaller insurers.

The fake gold came to light in February when Dongguan Trust (one of those infamous Chinese shadow banks) set out to liquidate Kingold collateral to cover defaulted debts. As the report continues, in late 2019 Kingold failed to repay investors in several trust products. To its shock, Dongguan Trust said it discovered that the gleaming gold bars were actually gilded copper alloy.

The news sent shockwaves through Kingold’s creditors. China Minsheng Trust - another shadow banking company and one of Kingold’s largest creditors - obtained a court order to test collateral before Kingold’s debts came due. On May 22, the test result returned saying the bars sealed in Minsheng Trust’s coffers are also copper alloy.

And with authorities investigating how this happened, Kingold chief Jia flatly denies that anything is wrong with the collateral his company put up. Well, what else could he say...

As Caxin notes, the Kingold counterfeiting case echoes China’s largest gold-loan fraud case, unfolding since 2016 in the northwest Shaanxi province and neighboring Hunan, where regulators found adulterated gold bars in 19 lenders’ coffers backing 19 billion yuan of loans, or about USD $2.5 billion. In that case, a lender seeking to melt gold collateral found black tungsten plate in the middle of the bars.

In the case of Kingold, the company said it took out loans against gold to supplement its cash holdings, support business operations and expand gold reserves, according to public records. It then appears to have decided to apply a gold-layer to tons of copper and pretend it was money-good gold collateral. And even more shocking, for years nobody checked the authenticity of the pledged collateral!

In 2018, the company beat a number of competitors in bidding to buy a controlling stake in state-owned auto parts maker Tri-Ring Group. Kingold offered 7 billion yuan in cash for 99.97% of Tri-Ring. The Hubei government cited the deal as a model of so-called mixed-ownership reform, which seeks to invite private shareholders into state-owned enterprises. But Kingold has faced problems taking over Tri-Ring’s assets amid a series of corruption probes and disputes involving Tri-Ring.

After obtaining the test results, Minsheng Trust executive said the company asked Jia whether the company fabricated the gold bars: “He flatly denied it and said it was because some of the gold the company acquired in early days had low purity,” the executive said. In a telephone interview with Caixin in early June, Jia denied that the gold pledged by his company was faked.

“How could it be fake if insurance companies agreed to cover it?” he said and refused to comment further. Well, the answer is simple: the insurance companies were in on the scam, but that's a story for another day.

In early June, Minsheng Trust, Dongguan Trust and a smaller creditor Chang’An Trust filed lawsuits against Kingold and demanded that PICC P&C cover their losses. PICC P&C declined to comment to Caixin on the matter but said the case is in judicial procedure. A source from PICC P&C told Caixin that the claim procedure should be initiated by Kingold as the insured party rather than financial institutions as beneficiaries. Kingold hasn’t made a claim, the Caixin source said.

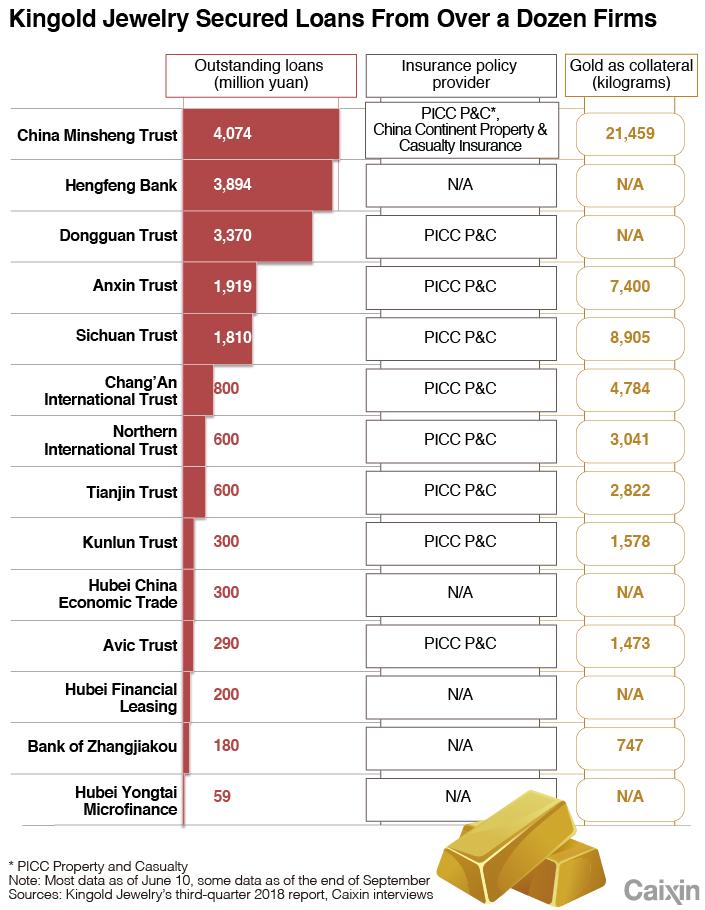

In total, Kingold pledge tens of thousands of kilograms of gold to no less than 14 creditors amounting to just under 20 billion yuan.

Caixin learned that the Hubei provincial government set up a special task force to oversee the matter and that the public security department launched an investigation. The Shanghai Gold Exchange, a gold industry self-regulatory organization, disqualified Kingold as a member as of last week.

Following Dongguan Trust and Minsheng Trust, two other Kingold creditors also tested pledged gold bars and found they were fake, Caixin learned. A Dongguan Trust employee said his company reported the case to police Feb. 27, the day after the testing result was delivered, and demanded 1.3 billion yuan of compensation from PICC P&C’s Hubei branch.

Meanwhile, Kingold defaulted on 1.8 billion yuan of loans from Dongguan Trust with an additional 1.6 billion yuan due in July.

The 83 tons of purportedly pure gold stored in creditors’ coffers by Kingold as of June, backing the 16 billion yuan of loans, would be equivalent to 22% of China’s annual gold production and 4.2% of the state gold reserve as of 2019.

In short, more than 4% of China's official gold reserves may be fake. And this assume that no other Chinese gold producers and jewelry makers are engaging in similar fraud (spoiler alert: they are.)

* * *

Founded in 2002 by Jia, Kingold was previously a gold factory in Hubei affiliated with the People’s Bank of China that was split off from the central bank during a restructuring. With businesses ranging from gold jewelry design, manufacturing and trading, Kingold is one of China’s largest gold jewelry manufacturers, according to the company website.

The company debuted on Nasdaq in 2010. The stock currently trades around $1 apiece, giving Kingold a market value of $12 million, down 70% from a year ago. A company financial report showed that Kingold had $3.3 billion of total assets as of the end of September 2019, with liabilities of $2.4 billion.

Jia, now 59, served in the military in Wuhan and Guangzhou and spent six years living in Hong Kong. He once managed gold mines owned by the People’s Liberation Army, which means he likely has connections all the way to the very top.

Jia Zhihong

Jia Zhihong

Jia Zhihong

Jia Zhihong

“Jia is tall and strong,” one financial industry source familiar with Jia told Caixin. “He’s an imposing figure and speaks loudly. He is bold, reckless and eloquent, always making you feel he knows better than you.”

Several trust company sources said Jia is well connected in Hubei - the epicenter of the coronavirus pandemic - which may explain Kingold’s surprise victory in the Tri-Ring deal. But a financial industry source in Hubei said Jia’s business is not as solid as it may appear.

“We knew for years that he doesn't have much gold ― all he has is copper,” said the source, who declined to be named.

Local financial institutions in Hubei have avoided doing business with Kingold, but they don’t want to offend him publicly, the source said. Why? Because of his extnesive connections with the Chinese army.

“Almost none of Hubei’s local trust companies and banks has been involved in (Kingold’s) financing,” he said.

That explains why most of Kingold’s creditors are from outside Hubei. Caixin learned from regulatory sources that Minsheng Trust is the largest creditor of Kingold with nearly 4.1 billion yuan of outstanding loans, followed by Hengfeng Bank’s 3.9 billion yuan, Dongguan Trust’s 3.4 billion yuan, Anxin Trust & Investment Co.’s 1.9 billion yuan and Sichuan Trust Co.’s 1.8 billion yuan.

But wait, counterfeiting gold is just the tip of the company's fraud iceberg: several industry sources told Caixin that the institutions were willing to offer loans to Kingold because Jia promised to help them dispose of bad loans.

Hengfeng Bank is the only commercial bank involved in the Kingold affair. The bank in 2017 provided an 8 billion yuan loan to Kingold, which in return agreed to help the bank write off 500 million yuan of bad loans, bank sources said. Kingold repaid half of the debts in 2018. But the loan issuance involved many irregularities as access to the pledged gold and testing procedures was controlled by Kingold, one Hengfeng employee said.

The loan was pushed forward by Song Hao, former head of Hengfeng’s Yantai branch. Song was placed under graft investigation in March 2018 in connection with the bank’s disgraced former Chairman Cai Guohua, whose downfall led to a major revamp in the bank’s management. In 2019, Hengfeng’s new management sued Kingold for the unpaid loans and moved to dispose the collateral. But a test of the gold bars found they are “all copper,” the bank source said.

It is still unclear whether the collateral was faked in the first place or replaced afterward. Sources from Minsheng Trust and Dongguan Trust confirmed that the collateral was examined by third-party testing institutions and strictly monitored by representatives from Kingold, lenders and insurers during the process of delivery.

"I still can’t understand which part went wrong," a Minsheng Trust source said. Bank records showed that the vault where the collateral was stored was never opened, the source told Caixin.

The falling dominos

Public records showed that Kingold’s first gold-backed borrowing can be traced back to 2013, when it reached an agreement for 200 million yuan of loans from Chang’An Trust, with 1,000 kilograms of gold pledged. The two-year loan was to fund a property project in Wuhan and was repaid on time. Before this, Kingold’s financing mainly came from bank loans with property and equipment as collateral.

It appears that one way or another, the company realized that it could fabricate gold ownership and receive money in exchange for what were basically worthless copper bricks painted as gold; and thanks to Jia's military connections nobody would ask any other questions.

As a result, starting in 2015, Kingold rapidly increased its reliance on gold-backed borrowing and started working with PICC P&C to cover the loans. In 2016, Kingold borrowed 11 billion yuan, nearly 16 times higher than the previous year’s figure. Its debt-to asset ratio surged to 87.5% from 43.4%, according to a company financial report. That year, Kingold pledged 54.7 tons of gold for loans, 7.5 times higher than the previous year.

It is now safe to assume that most of that gold never existed.

A person close to Jia said the surge of borrowing was partly due to Kingold’s pursuit of Tri-Ring. In 2016, the Hubei provincial government announced a plan to sell Tri-Ring stakes to private investors as a major revamp of the Hubei government-controlled auto parts manufacturer.

In 2018, Kingold was selected as the investor in a deal worth 7 billion yuan. According to the investment plan, Kingold’s purchase of Tri-Ring was part of a strategy to expand into the hydrogen fuel cell business, which is obviously a "logical" fit for a company involved in gold jewelry. Sources close to the deal said Kingold was attracted by Tri-Ring for its rich holding of industrial land that could be converted for commercial development.

Yes, at the very bottom of the fraud we finally get to the one true and endless Chinese asset bubble: real estate.

A Dongguan Trust investment document showed that Tri-Ring owns land blocks in Wuhan and Shenzhen that are worth nearly 40 billion yuan.

The deal drew immediate controversy as some rival bidders questioned the transparency of the bidding process and Kingold’s qualifications.

And here things get even crazier: according to Kingold’s financial reports, the company had only 100 million yuan of net assets in 2016 and 2 billion yuan in 2017, sparking doubts over its capacity to pay for the deal. Despite the fuss, Kingold paid 2.8 billion yuan for the first installment shortly after the announcement of the deal. The second installment of 2.4 billion yuan was paid several months later with funds raised from Dongguan Trust.

In December, Tri-Ring completed its business registration change, marking completion of Kingold’s takeover. However, the new owner has since faced troubles mobilizing Tri-Ring’s assets because of a series of corruption probes surrounding the auto parts maker since early 2019 that brought down Tri-Ring’s former chairman. As Caixin the notes, a majority of Tri-Ring’s assets were frozen amid the investigation and subsequent debt disputes, limiting Jia’s access to the assets.

The fraud is finally exposed

Hobbled by the Tri-Ring deal, which cost billions of yuan but has yet to make any return, Jia’s capital chain was eventually broken when Hengfeng Bank pushed for repayment, triggering a series of events that brought the fake gold to light, said a person close to the matter. Insurers’ involvement was key to the success of Kingold’s gold-backed loan deals. The insurance policies provided by leading state-owned insurers like PICC P&C were a major factor defusing lenders’ risk concerns, several trust company sources said.

“Without the insurance coverage from PICC P&C, (we) wouldn’t issue loans to Kingold as the collateral can only be tested through random picked samples,” one person told Caixin.

PICC P&C’s Hubei branch provided coverage for most of Kingold’s loans, Caixin learned. All the policies will expire by October. As of June 11, 60 policies were still valid or involved in lawsuits.

PICC P&C faces multiple lawsuits filed by Kingold’s creditors demanding compensation. But a PICC P&C spokesperson said the policies cover only collateral losses caused by accident, disasters, robbery and theft. Not fraud, and certainly not losses when the collateral never even existed!

Whose fault

Wang Guangming, a lawyer at Dacheng Law Offices, said the key issue is what happened to the pledged gold and which party was aware of the falsification. If Kingold faked the gold bars and both the insurers and creditors were unaware, the insurers should compensate the lenders and sue Kingold for insurance fraud, Wang said. Insurers are also responsible to compensate if they knew of Kingold’s scam but creditors didn’t, Wang said.

If Kingold and creditors were both aware of the fake collateral, insurers could terminate the policies and sue the parties for fraud. But if insurers were also involved in the scam, then all the contracts are invalid and every party should assume their own legal responsibilities, Wang said.

A financial regulatory official told Caixin that previous investigations of loan fraud cases involving fake gold pledges found there was often collusion between borrowers and financial institutions.

Earlier this year, PICC P&C removed its Hubei branch party head and general manager Liu Fangming. Sources said staff members involved in business with Kingold were also dismissed. PICC P&C said Liu’s removal was due to internal management issues. It didn't answer Caixin’s question about whether Liu was involved in the Kingold scandal.

PICC P&C’s Hubei branch provided insurance for most of Kingold’s gold-backed loans.

PICC P&C’s Hubei branch provided insurance for most of Kingold’s gold-backed loans.

* * *

The above story is shocking in exposing just how multi-faceted fraud is in China: capitalizing on pre-existing cronyism and connections with China's powerful army, the founder of Kingold was allowed to basically do anything he wanted, no questions asked, including counterfeiting over 83 tons of gold bars to get billions in funds to participate in China's housing bubble, only for a series of unexpected events to unwind the frauds one after another and expose the type of sordid scandal that is at the heart of most Chinese "enterprises" and business ventures.

As for the gold, yes - several billion in gold bars never existed and yet resulted in a cascade of subsequent cash flow events allowing tens of billions in funds to be released, "benefiting" not only founder Jia, but China's broader economy. Which is, needless to say, terrifying: because whereas just after the financial crisis China was engaged in building ghost cities, everyone knew these were a symbol of demand that would never materialize, even if the cities themselves did exist. However, it now appears that a major part of China's subsequent economic boom has been predicated on tens of billions in hard assets - such as gold - which simply do not exist.

As for what this means for the price of gold... well, Kingold is certainly not the only Chinese company engaging in such blatant fraud, and the consequences are clear: once Chinese creditors or insurance companies start testing the "collateral" they have received in exchange for tens of billions in loans and discover, to their "amazement", that instead of gold they are proud owners of tungsten or copper, they have two choices: reveal the fraud, risking tremendous adverse consequences and/or prison time, or quietly buy up all the gold needed to literally fill the void from years of gold counterfeiting.

Something tells us option two will be far more palatable to China's kleptoculture where one domino cold trigger a collapse of the entire financial system. What happens next: a panicked scramble to procure physical gold, one which even our friends at the BIS will be powerless to stop from sending the price of the precious metal to all time highs.

No comments:

Post a Comment