This is an item we have seen before,but it is well worth grinding through for the education. What is unfortunate is that it is all a mass of agreed upon ideas and beliefs that a handful of individuals assign credence to.

I do not wish to say it is all wrong but it is deeply flawed because it fails to directly resolve poverty asn economic problem. In fact, it sustains poverty for no good reason except for idle excuses.

Understand that the globe can sustain a measured eight percent growth rate while initially eliminating all poverty outright. Interest can be earned and paid.

What happens though is that the base strengthens and become broadened to include the whole of humanity, including even the folks managing large amounts of their own capital

Currency, Credit, and Usury as a Control Mechanism

Operation Disclosure | By David Lifschultz, Contributing Writer

Submitted on July 8, 2022

CURRENCY, CREDIT AND USURY AS A CONTROL MECHANISM

COMPLIMENTS OF THE LIFSCHULTZ ORGANIZATION FOUNDED IN 1899

Though this paper was written almost a decade ago, it is more urgent in 2007 about the evil usurpation of power by the fraudulent global economic practice of usury.

Currency, Credit and Usury as a Control Mechanism 1

(author anonymous)

Who hold the balance of the world? Who reign

O’er congress, whether royalist or liberal?

Who rouse the shirtless patriots of Spain?

(that make old Europe’s journals squeak and gibber all).

Who keep the world, both old and new, in pain

or pleasure? Who makes politics run glibber all?

The shade of Bonaparte’s noble daring?

Jew Rothschild and his fellow Christian Baring.

From Don Juan of Lord Byron

Here we have the most interesting and accurate analysis of the power transfer of inflation ever presented in the English language. But the Germans are not far behind.

Chancellor

In my old days my happiness how great!

Hear, then and see this fateful scroll, for this

Has turned our woe and wailing to bliss.

“Be it to all whom it concerneth known,

This note is worth a thousand crowns alone,

And for a guarantee, the wealth untold,

Throughout the empire buried, it hath hold.

Means are on foot this treasure bare to lay.

And out of it the guarantee to pay.2

Emperor

Crime I surmise, some monstrous fraud. Oh shame!

Who dared to counterfeit the Emperor’s name?

Here Goethe explains what William Paterson, the founder of the Bank of England, said in 1694 that “The Bank hath benefit of interest on all moneys which it creates out of nothing.”4 The Emperor considers it a fraud. Shortly after, Goethe predicts the overthrow of Christianity and the nobleman whose duty it was to defend it by this new banking power. Since we do not have statistics available for the 1819-1832 period during which Faust and Don Juan were written, we cannot analyze this power transfer from the clergy and nobleman to the bankers except to show it by modem statistics. The United States presently has 11.050 billion in gold at 42.22 per ounce against about 4 trillion in paper currency, coin and credit which represents M-3 of 4.744 trillion less an estimate for non-depository instruments. All American statistics will be taken from the Federal Reserve Bulletin of November 1996. The inflation level would represent 4 trillion less 11.050 billion in gold if we wish to use an unconventional definition of inflation as representing the excess of currency and credit above the gold reserve.

It is interesting to follow how this credit is manufactured out of thin air. I will only give a rough approximation on how this is done. The Federal Reserve supplies most of the funds out of about nearly 400 billion in Treasuries it acquired merely by transmitting a credit balance to a bank (manufactured out of thin air). This supply of funds represents one side of the balance sheet. The other side is described as use of funds or absorbing reserve funds. Here we have as a use currency in circulation, part of which is used for vault cash at the banks, and reserve balances at Federal Reserve Banks (Page A-5 of Bulletin). Vault cash plus reserve balances at Federal Reserve Banks constitute the 0% to 10% required reserves of the banks (Page A-8) of 52.26 billion (page A-12). These are the raw requirements of the system. The question is how does the 400 billion Fed credit become 4 trillion. If we took the 52.26 billion reserve requirement at the .03% reserve ratio for transaction accounts under 52 million (A-8) we come out to 1.742 trillion expansion, still short of 4 trillion. But some of the reserve ratios are 0% for non-personal time deposits, savings accounts, and eurocurrency liabilities.5 The expansion at 0% can make up the difference since we must also consider as a use nearly 429 billion in currency.6 The way a reserve ratio works is if the Federal Reserve creates, out of thin air, 40 million credited to an account in a commercial bank to buy a Treasury Bill, the bank can lend out 38.8 million, holding a 3% reserve of 1.2 million. When the 38.8 million returns to the banking system, it can re-lend it out 37.636 million, holding 1.164 million as a 3% reserve. When this process expands out, the 40 million becomes 1.333 billion of loans. This calculation can be expressed in the simple algebraic formula 0.03x = 40 million, with “x” representing the total amount after the expansion. Consequently, the banks create out of thin air credit in the amount of 1.293 billion dollars (1.333 billion less 40 million). The system is a closed circuit, as no credit leaves it to foreign countries to pay the balance of payment deficit. What happens is the credits are bid for in the foreign exchange market. When the U.S. incurs a deficit, a credit to a foreign bank appears in the account of the U.S. bank. If the foreign bank wishes to sell the U.S. deposit, his account is debited, and the buyer of the dollars will have his American bank credited. If there were no market for these credits, the U.S. dollar would fall until there was one. Foreign central banks will often intervene to buy such dollar deposits or credits and then use them to purchase Treasury Bonds. Their holdings amount to 572.839 billion in June and mostly reflect the massive efforts of the so-called Asian miracle economies to support the dollar to facilitate the continuation of massive U.S. trade deficits. This currency manipulation is described as a dirty float.7 The Eurodollar market is like re-used toilet paper. The European bank has a deposit of dollars in a U.S. bank from which it creates new loans on its own books without any reserve requirements. This additional expansion of credit is huge.8

The gross domestic product is about 7.547 trillion dollars (Bulletin, p.48). So if we compare 4 trillion in currency and bank credit, we can see the stupendous transfer of power to the privately owned banks. Byron attributed this new power in his time to Rothschild and Baring and Goethe’s Mephistopheles is Rothschild. Goethe obviously considered this inflation a fraudulent hypothecation of the original gold reserve which today, if it were used on any other asset such as real estate, would be regarded as a criminal fraud. In any event, this fraudulent banking power through their endowments to universities selected their presidents and changed their curriculum away from Christianity, which taught against usury, and away from the study of classics such as Aristotle, since this undermined the banker’s position in society from that of honored citizens to their original status of guttersnipe.9 Newspapers under their influence in the U.S. were the N.Y. Times, N.Y. Herald Tribune, Christian Science Monitor, Washington Post and the Boston Evening Transcript. See for this source Carroll Quigley’s Tragedy and Hope, pp. 952-3 and 980. Although this subject is given vast treatment throughout, Mr. Quigley does not draw the obvious Christian implications. This dechristianization was achieved through this stupendous transfer of wealth and power by which the privately owned banks (and the Federal Reserve is nominally privately owned, for that matter, though highly regulated and most of its interest income is returned to the Treasury) were enabled to create out of thin air nearly four trillion of deposits less currency. How many Americans understand this, much less received the opportunity to vote on it? Mr. Quigley basically tells us our American democracy is a banker’s stage on which the politicians, their marionettes, dance. The pirouetting judges are merely the agents of the politicians. Byron justly said they “make politics run glibber all” and make “Europe’s journals (newspapers) squeak and gibber all.” One need only have watched the massive orchestration behind Nafta and Gatt to be convinced.

When I read through the various Federal Reserve, International Money Fund, and Bank for International Settlement, material in preparation for this report, I was surprised at the influence of the stockbroker, David Ricardo, through his analysis of comparative advantage and inflation. His definition of inflation is found in his 1810 piece entitled “The High Price of Bullion, A Proof of the Depreciation of Bank Notes.” He wrote if too many pounds were issued there would be an inflation causing gold to rise in value and the pound to fall. His remedy was to withdraw pounds from circulation. This would be done today by the Federal Reserve selling Treasuries taking back and extinguishing previously created credit. Today the Ricardian definition of inflation is the rise in the price of goods instead of gold in relation to the paper money and credit. This is measured by the Consumer Price Index. I use a study on this inflation entitled: The U.S. Dollar = An Advance Obituary by Dr. Franz Pick. Here are his inflation figures reflecting the erosion of the dollar’s value through inflation, starting at 100 in 1940 . . .

The inflation wiped out 86.9% of the government index since 1940 and around 96.5% to 97% in the unofficial statistics. Dr. Pick relates in his book that he never changes the commodities in his unofficial commodity baskets while the government does. The U.S. government’s policy is that if a product becomes very popular, its price rises causing it to be bought by much fewer people and so its importance in the economy decreases. So it drops it from its basket. Dr. Pick says this thereby understates true inflation. He never changed his basket since 1940. The destruction of 86.9 to 97 per cent of the 1940 dollar is a reflection of the fraudulent transfer of wealth. Since much more inflation has occurred since 1985, the figures today are worse.

We can now understand why he entitled his book The U.S. Dollar: An Advance Obituary because Dr. Pick was predicting the dollar’s future death. Rene Sedillot wrote in Paris in 1954: “It will come to a bad end”, repeated Jacques Bainville’s parrot in Jaco et Lori. “In the cases of currencies, alas, it always ends badly.” 10

Now, why is this so? In The Merchant of Venice by Shakespeare, Antonio asks “…is your gold and silver ewes and rams?” This is reminiscent of Aristotle in Politics 1:3:23.

“But, as we said, this art is twofold, one branch being of the nature of trade while the other belongs to the household art; and the latter branch is necessary and in good esteem, but the branch connected with exchange is justly discredited (for it is not in accordance with nature, but involves men’s taking things from one another). As this is so, usury is most reasonably hated, because its gain comes from money itself and not from that for the sake of which money was invented. For money was brought into existence for the purpose of exchange, but interest increases the amount of money itself (and this is the actual origin of the Greek word: offspring resembles parent, and interest is money born of money); consequently this form of the business of getting wealth is of all forms the most contrary to nature.”

Now what does Aristotle mean by contrary to nature? If we have in an economy 100 million ounces of gold lent at 10% interest, the 100 million ounces cannot breed the extra 10 million ounces, so defaults to the lenders will occur. Wealth will concentrate in the hands of the lenders.11 If we try to escape this discipline through fraud as in Goethe’s and Byron’s time, paper money and bank credit in excess of the gold will be created provided (if we follow Ricardo) the price of gold doesn’t rise (inflation). Discipline, however, is nearly impossible to maintain for if the amount of credit is not continuously increased to pay the interest, the same defaults will occur as if we had a finite amount of gold. As the inflation of paper units and credit continues, the ratio of gold to paper decreases even if the consumer price indexes are not increasing. This ratio of gold as it decreases makes the convertibility of the currency into gold impossible. In the case of international or domestic runs, the currency unit will default or die as the central bank will not have enough gold to cover the withdrawals. If the monetary authorities attempt to deflate the currency to a 100% gold backing, untold human hardships will follow as the economy goes into a depression. This is usually avoided as otherwise a revolution will occur.

The final solution of modern times to this problem is to declare gold a barbarous relic and just trust in paper money. Here we have a kind of neoplatonic transubstantiation of a paper or credit unit (with no gold backing or intrinsic value) into an energy (Karl Marx) or a value (David Ricardo).12 The truth is that this transformation is merely a sleight of hand to conceal the fraudulence and unworkability of the system. The credit and usury system is the barbarous relic from the fallen nations of antiquity. (See Annals of Tacitus, Book 6, 16). Even without the gold base, the growth of paper and credit must grow continuously to pay the interest. Only an omniscient mind can control the domestic credit issuances in relation to its floating against other currencies, which in the end will be mathematically or statistically impossible (see Gen. 3:5). If we use our four trillion of currency and credit outstanding as a proxy, and allow a 6% average interest figure, recognizing the cyclical nature of interest rates due to occasional efforts to control this syndrome, we list below the credit figures after compounding annually.

25 years 17 trillion

50 years 74 trillion

75 years 316 trillion

100 years 1,357 trillion

213 years 1,000,000,000,000,000.0013

It is true we have allowed about 425 billion in currency in the above calculation, which is in circulation, but our interest rate is low as most bank loans are above 8%. Our point is that 25 or 50 years from now the monetary authorities (not being omniscient) will not be able to manage this. They must, however, keep increasing the money supply at least by the interest rate or the system will contract and collapse. As we saw in Dr. Pick’s inflation history, they were unable to restrict the money growth sufficiently, thereby creating an enormous historical inflation, even against the consumer price index. This does not give us confidence in the future that the Federal Reserve will not significantly exceed our 6% interest proxy. At some point between now and 50 years, our currency and credit system will explode. If we review Dr. Pick’s inflation history between 1940 and 1985, nearly 97% of the dollar’s value was destroyed. Costantino Bresciani-Turroni in his The Economics of Inflation writes that in 1781 the American “continental money” was worth only a thousandth part of it original value. The depreciation of the French assignats on June 1, 1796 was one metal Franc to 533 assignat Francs. The gold mark in 1913 was equal to one paper mark, whereas in 1923 one gold mark equaled 1,000,000,000,000 paper marks. At what point will the U.S. system self-destruct as in 1796 France, 1781 America, or 1923 Germany? When we remember the U.S. has 11.050 billion in gold, it is scheduled to underpin 74 trillion in dollars and credit in 50 years. The chief difference between the U.S. situation and the German one is the time span, not the currency and credit mathematics.14 In the U.S. the same gigantic abstraction of the currency will occur but over a longer time. The illogical nature of the system is understood by few.

I have saved for last some discussion of the use or manipulation of the inflated unit for political and economic power. Mr. Quigley in his books tells us the Rothschild House “manipulated the quantity and flow of money so that they were able to influence, if not control, governments on one side and industries on the other (page 51 Tragedy And Hope).15 What he means is that if a government gave the Rothschild’s trouble, they would deflate the credit system, thereby overturning it . For example, Mr. Quigley asserts that J. P. Morgan engineered the “panic of 1907” (p. 72). This was probably done to get us into the Central Bank system of a Federal Reserve. It would be easier to control the U.S. economy through this mechanism as was seen in the 1928-33 tightening. Blame is deflected from the private bankers.

Let’s turn to an example. Between 1928-30 there was a Republican tariff movement in the U.S. whose purpose was to protect American Industry. In 1930 they passed the Hawley-Smoot Tariff Act. Since tariffs interrupt bank credit flows, the U.S. Federal Reserve under orders from Baron Eduard de Rothschild in Paris restricted credit between 1929-1933 for the purpose of overturning Republican tariff control of the U.S.16 Rothschild’s men17 on the Federal Reserve strangled the U.S. and in 1932-33 the Democrats won a resounding election, taking over the presidency and both Houses of Congress. Baron Eduard accumulated huge gold holdings in Europe and, in the heart of the depression in the U.S., ordered the Paris Central Bank to start a run on the U.S. gold supply. (Tragedy and Hope p. 349) states the French Central Bank started the run. The Rothschild President, F. D. Roosevelt, used this as an excuse to reward his patron by devaluing the dollar in a deflation (a very rare event in history, as this virtually always happens in an inflation) and then the good Baron converted his gold into dollars, buying up depressed U.S. assets, thereby making a killing.

Farfetched? Is it likely that the J. P. Morgan firm was independent of Rothschild and Rothschild had no major presence in America, though the towering giant in Europe?18

Dr. Pick said Morgan took orders from Rothschild and profits were skimmed to Rothschild from the Morgan firm, as the Las Vegas Casinos do to their Mafia overlords.19 Lets look at pp. 326 and 327 in Quigley’s book . . .

“It must not be felt that these heads of the world’s chief central banks were themselves substantive powers in world finance. They were not. Rather, they were the technicians and agents of the dominant investment bankers of their own countries, who had raised them up and were perfectly capable of throwing them down. The substantive financial powers of the world were in the hands of these investment bankers (also called ‘international’ or ‘merchant’ bankers) who remained largely behind the scenes in their own unincorporated private banks.”

The monetarist Milton Friedman, in explaining the 1929-33 monetary contraction, wants us to believe that these banking specialists were just inept.20 This is hard to swallow, as these fellows were experts. The Rothschild-Roosevelt story outlined here was related as true to a relative by Dr. Franz Pick, Baron Eduard de Rothschild’s selection as paymaster of the French Resistance. But whether it is true or not, and we have no doubt it’s true, is not as important a question as to what must we do now.

We close by saying that acceptance of the Bible’s prohibition against usury and fraudulent hypothecation would have prevented these massive credit upheavals of our century. And then there could have been no rise of psychopathic personalities, as Joseph Stalin and Adolf Hitler. The good book is still good. (See Ex. 22:25; Lev. 25:36,37; Deut. 23:19,20; Deut. 25:15; Lev. 19:36).

We have scientifically demonstrated that the interest rate system was unworkable and doomed. Here we shall show how it is the ferment of decomposition of our western civilization.

The major pressure driving the United States and the world economy is the interest rate burden. Although page A-41 of the April Federal Reserve Bulletin shows 19.5 trillion in credit market debt and 43,325 trillion in total liabilities, most of this nets itself out, as often the lender to one party is the borrower from the same party. For example, I could buy a Sears bond, on the one hand, and buy on credit from Sears on the other. Both liabilities would be picked up and aggregated. The best measure of the interest rate burden is the 193 billion (1996) net interest21 which represents the difference between the interest on loans of financial intermediaries and their cost of funds. This 193 billion net interest compares to 249.3 billion of 1995 personal savings and 586.6 billion of 1995 corporate profits.22 The interest rate burden was the source of the historical financial pressure that uprooted the old agrarian economy and drove our civilization to the speed-up of contemporary life. It drives the frantic race to greater efficiency to service the interest, and is the main source of technological innovation, automation and greater industrialization.23 The remaining farms have been turned into factory systems. Here unhealthy chemical fertilizers are used to boost production, which destroy the bacteriological balance, necessitating pesticides. These substances cause a deterioration in the national health and lead to cancer. Hormonal treatment of cattle and poultry to grow faster and pump up the egg production also contribute to cancer.

The mad chase to greater efficiency is supposed to lead us to a modern paradise where machines do all the work and leisure abounds, but instead has led to the masses having to live in squalid, ugly cities that are as barren and sterile as deserts. The quality of life in the cities is far inferior to the old agrarian civilization, and the modern glass architecture is insubstantial and ugly. When driving out of this wasteland, the eyes are affronted by concrete, gas stations and Coca-Cola signs. Modern civilization’s attempts to escape arduous work (Gen. 3:19) by the sweat of the brow (healthy exercise) has led to the loss of the beautiful bucolic world of pasturage and farming where families had many healthy children and strong rugged men.

The average modern man is in hock for his home mortgage, car loan, and consumer loan and worries that his good paying job with a one-month vacation will be wiped out by imports or immigrants. He must worry that his frustrated children may develop passions for degenerate movies or disreputable rock stars that represent our new culture, but really serve as distractions to meaningless lives. The financiers are happy if we don’t recognize their sordid system, as they promote this moral disintegration.

It was not always so. Peter Jon Simpson in a pamphlet entitled Life Without Usury quotes from Thorold Rogers, Professor of Political Economy at Oxford University in the middle of the nineteenth century that “at that time (in the Middle Ages) a labourer could provide all the necessities for his family for a year by working 14 weeks.” For this the bankers had him fired.

Werner Sombart in his study of agricultural conditions in Central Europe in the fourteenth century “found hundreds of communities which averaged from 160 to 180 holidays a year.” Here was old “Merrye Englande.” That free time was used to build beautiful Gothic cathedrals.

Their crowds didn’t sit before the television watching insulting vulgarity but went a different way.

And specially from every shrines end

Of Englande to Canterbury they wende

The holy blissful martyr for to seeke

Them that hath holpen when that they were seeke.

Who is really superstitious? The modern man who believes that paper money or bank credit has value when it has no intrinsic value, or these noble English folk who had half a year off to build Gothic cathedrals or go to shrines to venerate saints who resisted temptation? (Our movies glorify whores.) Their money was gold and silver, or agrarian goods. Real goods.

The incessant propaganda of the financially controlled media would have us believe this bucolic world never existed – and that medieval farmers were lazy, loafing dolts. But our world isn’t even a debased copy of theirs.

If we had adhered to the Biblical prohibitions against usury, our world would not have been ruined by the fangs of international finance capital. They have brought ruin to our world in two world wars and are setting the stage for another collapse outlined in “Deficit Without Tears”. We must return to God and His Bible25 and take back our Western civilization from the international financiers. The good book, dear reader, is still good.26

Bibliography

1. The Jews And Modern Capitalism, By Werner Sombart, translated by M. Epstein, Transaction Books, New Brunswick, U.S.A., 1982.

2. Federal Reserve Bulletin, November 1996, Board of Governors of The Federal Reserve System, Wash., DC

3. Works of Lord Byron, London: John Murray, Albermarle street, 1833, Vol. 17, Don Juan.

4. Confessions of The Old Wizard, by Dr. Hjalmar Horace Greeley Schacht, Houghton Mifflin Co., Boston, 1956.

5. Tragedy And Hope, Carroll Quigley, 1966, The Macmillan Co., N.Y., (President Clinton’s favorite professor at Georgetown University).

6. Modern Money Mechanics, Federal Reserve Bank of Chicago., Feb 1994

7. Settlement Risk In Foreign Exchange Transactions, Bank For International Settlements, Basle March, 1996

8. Central Bank Survey of Foreign Exchange And Derivative Market Activity, Bank for International Settlements, Basle, May, 1996.

9. Politics, Aristotle, Loeb Classical Library, translated by H. Rackman, Reprinted 1990. Book 1,3,23, Loeb page 51.

10. The Tragedy of Faust, by J. W. von Goethe, translated by Sir Theodore Martin, Boston, Francis A. Niccolls and Co., Publishers, 1902.

11. The High Price of Bullion, A Proof of The Depreciation of Bank Notes, Second Edition corrected, by David Ricardo, London, Printed for John Murray, 32 Fleet-street., 1810.

12. The Merchant of Venice, by William Shakespeare, Macmillan and Co. London, 1891, The Works, Act 1, Scene 3, verse 90.

13. The U.S. Dollar: An Advance Obituary, Third Edition, by Dr. Franz Pick, 1986, Pub. by Silver and Gold Report, Bethel, CT 06801.

14. All The Monies of The World, by Franz Pick-Rene Sedillot, Pub. by Pick Publishing Corp., N.Y., N.Y. 10006, 1971

15. The Economics of Inflation, by Costantino Bresciani-Turroni, translated by Millicent E. Savers, Augustus M. Kelley, Publishers, Third Impression, 1968.

16. International Monetary Fund Yearbook, 1996, International Monetary Fund, Washington, D.C.

17. A Monetary History of The United States, by Milton Friedman and Anna Jacobson Schwartz. Published by the National Bureau of Economic Research, Eighth Paperback printing, 1990

18. Direction of Trade Statistics Yearbook, 1996 International Monetary Fund.

19. Fedwire March 1995, Federal Reserve Bank of New York.

20. International Banking and Financial Market Developments, Bank for International Settlements, Basle, November 1996.

21. The Annals, by Gaius Cornelius Tacitus, The Loeb Classical Library, John Jackson, translator, 1986.

ENDNOTES

1 This essay was inspired by Dr. Martin Luther’s Trade And Usury.

2 Works of Lord Byron, London : John Murray, Albermarle Street, 1833, Vol. 17, p. 41.

3 The Tragedy of Faust, Part 2, pp. 283-4, by J. W. von Goethe, translated by Theodore Martin. Dr. Hjahnar Schacht’s Oct. 15,1923 Rentenmark (revenue mark) used Goethe’s analysis in the invention of this new currency by its being “guaranteed by gold mortgage on all German lands, by gold obligations of industry, commerce and banks” even though the real gold cover was nearly nonexistent. See page 164 of Dr. Schacht’s Confessions of the Old Wizard, and pages 323 and 472 of Dr. Franz Pick’s and René Sedillot’s All The Monies of The World. This created out of thin air Rentemnark and worked like a miracle to end the German hyperinflation of 1923. Goethe described this Rothschild technique a few pages further in Faust, Part 2, as “all heretics’ and wizard’s doing.”

4 Tragedy and Hope, p. 49, by Carroll Quigley.

5 Those who say that deposits under zero reserves can extend out to infinity are philosophically and practically wrong. On a practical basis, the bank’s necessity of holding “working balances” would at the very minimum prevent the extension to infinity. Infinity, as it relates to man’s finite intellectual capacity, is an absurd concept outside of theology.

6 The supply of funds and the use are equal. However the November Bulletin statistics don’t always balance, as figures appear from different times. Information developed by telephone inquiry with the Fed.

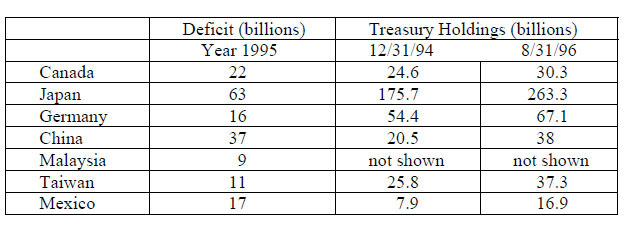

7 The dirty float issue is pregnant with meaning. In 1995 the U.S. had a 187 billion trade deficit with the following significant trade deficits with individual trading partners.

The figures of Treasury holdings for each of these countries sheds light on their intervention in the market, preventing the self-correcting mechanism of supply and demand of dollars to lower the value of the dollar irrespective of purchasing power parity. Foreign holdings now represent 30% of total privately held public debt. Figures taken from Direction of Trade Statistics Yearbook 1996 of the International Monetary Fund, and Quarterly Press Conference of November of Asst. Secretary of Domestic Finance, Darcy Bradbury.

A large support for the dollar against the Yen is the Japanese subsidized half a percent central bank rate to relieve their beleaguered banks, which has generated one of the largest speculative manias in the history of Wall Street, sending average stock yields to their lowest level in 100 years. What is happening is that hundreds of billions are being borrowed in Japan at low interest rates and then invested in the U.S. in Treasuries at higher yields in a classic arbitrage operation. This artificially lowers interest rates in the U.S. sponsoring the stock market. Senior central bank officials expressed their concern about these developments but feel the Japanese must reflate their banks. Shall it result in an uncontrollable financial crash? In the meantime, the Japanese exporters to the U.S. are having a heyday with the high U.S. dollar.

Some argue that the 1995 trade deficit is inconsequential, as it represents only 2.5% of the U.S. Gross Domestic Product (187 billion out of 7.5 trillion). However, this forgets about the inequity of the dirty float and the significant composition of industrial products, such as cars and steel, that these imports represent and how such attacked industries have been in periodic distress. Imports now account for about 28% of our car industry and a significant portion of our steel industry. It must be remembered that the power of a modem nation is found in its power of production (see Tacitus Annals, Book XII, p. 43).

What we see happening is whenever another country has a problem, such as the Mexican debacle, the U.S. surplus of 5 billion in 1992 is turned into a deficit of 17 billion in 1995 to solve the problem. Or Japan’s bank problems, stemming from the crash of their crazed real estate and stock markets, require our acceding to their low interest rates which exacerbated the U.S. – Japanese trade deficit. Japan’s speculations were symptoms of excessive trade surpluses and excessive industrialization, and attempts by the Japanese central bank to encourage and discourage surpluses resulting from alternating foreign pressures. In any event, the U.S. has in the last 12 years switched from a net creditor nation in 1984 to a not inconsequential debtor nation, to the tune of 773.65 billion dollars (Balance of Payments Statistics.Yearbook,1996, International Monetary Fund).

This 773.65 billion does not tell the whole story, however. Federal Reserve and U.S. policy is held hostage to a 1.9 trillion foreign portfolio investment consisting of equities and debt securities. In 1995 alone 192.38 billion poured into U.S. equity and debt securities. The great fear that our authorities have is that this investment will be sold if the dollar were to fall, so they are quite prepared to sacrifice American industry by supporting a strong dollar, through manipulation, to avoid a panic. But it was the artificially propped up dollar in the first place that brought us to such a pass. These manipulations, of course, are facilitated by the inflation of currency and credit. (Statistics obtained from the Balance of Payments Statistics Yearbook, 1996, International Monetary Fund).

8 It is estimated that the Eurodollar market in 1973 was 73 billion, in 1980 500 billion, and in 1988 1 trillion. These are gross figures, due to multiple counting of cross-bank deposits. The net figure in 1988 might have been 333 billion, although today it is significantly more. Morgan Guarantee Trust is the source for the figures through 1988 and Federal Reserve Source. The November 1996 Bank for International Settlements “International Banking and Financial Developments” shows a present Eurodollar sum of 3.180 trillion which our Fed source would divide by 3, but the B.I.S. would divide by about two, to net out interbank deposits.

9 It is important to note that these Rothschild actions undermined the religious faith of their own people as well.

10 All The Monies of The World, by Franz Pick-René Sedillot, 1971, Pick Publishing Corp., N.Y., N.Y. 10016

11 If mined gold is growing at 2% it cannot furnish the 8% liquidity deficiency (10% less 2%). The same principle applies to a world system.

12 O Gold! I still prefer thee unto paper, Which makes bank credit like a bark of vapour. (From Don Juan Byron, vol. 17, p. 4. Also see 2 Thessalonians 2:10-12).

13 Some will say that inflation is the originating source that drives this interest rate up. But this ignores history and economic logic. Before the credit system was extensively developed in Europe, the scarcity of gold drove its interest rate to grand heights (at times in the early middle ages 30% figures are recorded and higher). This demand for gold also drove the alchemist into frantic studies to convert base metal into gold. It was the substitution of paper currency and credit for gold that drove interest rates down by increasing the supply of these gold substitutes which was not inflationary in a Ricardian sense as long as the loans were linked to productive investment. (History teaches, however, that the severe discipline required to maintain this linkage always breaks down. We need only survey the unproductive borrowing for pure speculation of today’s financial buccaneer, George Soros). A tremendous artificial prosperity followed, as Goethe tells us in Faust, Part 2 . . .

“A few strokes of thy pen, and so thou’ It seal,-

This revels crowning joy, – thy people’s weal!”

These strokes thou mad’st, which were ere morning-tide.

By thousand hands in thousands multiplied.

That all alike the benefit might reap,

We stamped the whole impression in a heap;

Tens, thirties, fifties, hundreds, off they flew-

You can’t conceive the good they were to do.

Look at your town, – t’was mouldering and half dead-

Now all alive, and full of lustihead!

High as thy name stood with the world, somehow

T’was never looked so kindly as now.

The list of applicants fill to excess;

This scrip is rushed at as a thing to bless.

If Germany had listened to Goethe, the overthrow of their civilization would not have occurred and they would have avoided the currency and credit calamities of 1920-1933, which were the final consequences of the fraudulent hypothecation. “For you spreads Satan’s golden snares; you’ll do what is unrighteous and unholy, too.” And though the final consequences of unholy actions can be long in coming, they come.

14 This system is prone to other grave risks. There is 1.2 trillion dollars daily trading in foreign exchange markets in an estimated 7 trillion yearly world trade of goods and services (5 trillion of 1995 goods yearly traded per I.M.F. Yearbook 1996, and an estimate on services. U.S. exports and services were 786 billion in 1995). This exposes large trading banks to significant exposures in relation to their net worth in the event of a default of a bank trading partner in another country. Citicorp, for example, shows only 7.6% (19.581 billion) equity and a 16 billion foreign exchange contract exposure before netting agreements in their 1995 Annual Report. A major trading bank default can cause a major chain reaction of defaults. There is no established lender of last resort mechanism covering foreign exchange transactions or insurance as in the case of bank deposits under $100,000.00 insured in the U.S. by the Federal Deposit Insurance Corp. The huge foreign exchange markets trade far in excess of actual real trade (1.2 trillion per day versus 7 trillion world trade per year) as the abolition of fixed exchange rates with currencies linked to gold (its collapse was inevitable, as this paper explains) forced companies in world trade to hedge their commercial transactions in future currency markets to be sure their sales in marks or yen would have the same value in the future as when the sale was made.

Pure speculation also contributes to these figures but the B.I.S. has no such figures available or estimated. See March 1996 and May 1996 Bank for International Settlement Reports entitled “Settlement Risk In Foreign Exchange Transactions” and “Central Bank Survey of Foreign Exchange and Derivatives Market Activity”, respectively. Conversations with authorities at the Federal Reserve at New York and the Bank for International Settlements in Basle, Switzerland revealed that for the most part the 1.2 trillion daily foreign exchange market was a black hole to them, and that the Federal Reserve in N.Y. restrained them from making a more extensive study. The B.I.S. estimates six transactions in the future market relating to manufacturer’s trade hedging for each trade transaction. If we say that there are 260 working days in the year, and 1.2 trillion daily trading in dollars in the foreign exchange market, then annual foreign exchange trading will amount to 312 trillion. The ratio to world domestic product calculated on value added accruals would be 10.776 on a 28.953 trillion world domestic product (312/28.953). The ratio on world trade (not an end product figure) in services and goods, which is a gross transactions total, would be 44 on an estimated 7 trillion in directional trade or 312 divided by seven. Since the B.I.S. estimates 6 hedges, it leaves 38 trades unaccounted for, or 13.6 % (6/44) accounted for.

If we examine the Fedwire transactions we find a daily turnover of 841 billion per day in 1994 on a gross domestic product of nearly 7 trillion. When we use the 218.66 trillion figure (260×841), then the ratio is 31 (218.66/7). Since 7 trillion G.D.P. only represents the total value added, or end product value, the 218.66 trillion would represent gross underlying domestic transactions relating to this seven trillion G.D.P.

If we examine The Clearing House Interbank Payments System, or CHIPS, we find in the January 1991 report of the Federal Reserve of N.Y. that about one trillion of payments were handled by offset between the members with the balance at the end of the day settled by Fedwire. “82% of CHIPS’ dollar volume of payments resulted from foreign exchange transactions or Euro-dollar placements (pages 1 and 9 of report).” When we search for what this N.Y.C. turnover consists of we must make a broad survey. The total valuation of the N.Y.S E. is 7.3 trillion dollars with 4.1 trillion trading annually (U.S. G.D.P. about 7.5 trillion dollars). If we divide 260 trading days into 4.1 trillion, we come out to 157 billion per day trading. Nasdaq total valuation is 1.5 trillion with 3.3 trillion trading annually. The American Stock Exchange total valuation is 126 billion with 91 billion trading annually. Federal debt amounts to 5.2 trillion although turnover figures are not shown on available reports. On page A-41 in the Federal Reserve Bulletin there is 19 trillion of various debt holdings listed, and it is in here as well as in the stock markets that most of the one trillion daily CHIPS transactions are composed. Some of these debt instruments will trade in multiples daily and others not at all. It is questionable on the basis of economic utility whether a large part of this turnover, or churning, can be regarded as socially useful.

There is thus a direct connection between the Fedwire and CHIPS transactions and the turnover on the foreign exchange markets, and a large part of the 1.2 trillion daily trading on the foreign exchange market relates to N.Y. security and bond trading. Thus severe stock and bond market fluctuations in N.Y. can be instantaneously translated through the foreign exchange market with tidal wave force. (Data obtained from IMF Direction of Trade Statistics Yearbook, 1996, the March 1995 Federal Reserve Bank of NY, “Fedwire,” Bank for International Settlements, and Swiss bankers).

It is difficult to analyze where stock selling could engender a panic because of black holes in data. There is over 90 billion in bank margin lending for individual stock purchases at up to 50% margin, which is in itself not overly large when you consider the total valuation of the N.Y.S.E. alone of over seven trillion (or about the same as the entire G.D.P). It is more difficult to analyze exposures in option and derivative markets which periodically surface in Orange County debacles through lack of information generated by regulatory authorities. (These same authorities refused to even subpoena the relevant transaction data after the manipulation in the cash settlement market precipitated the 1987 stock market crash). Wall Street’s senior executives have expressed deep concern on this subject.

Another area where information is deficient is the purchase of stocks here by foreigners on foreign borrowings and borrowings by foreign domiciled hedge funds. Huge stock market participation of mutual funds, consisting largely of funds of inexperienced investors without time withdrawal requirements, are more obvious areas for massive panic selling in a mushrooming stock market decline. The sophistication of the managers of pension funds is highly in doubt when one only briefly reviews the Orange County catastrophe, and more especially when one looks at their high percentage of stock market exposure with yields at 100 year lows below 2% (average yields on stocks over 100 years were 4%, and has been as high as 6% which latter figure could presage a significant fall in stock indexes). The suggestion that the salvation of the Social Security System is to be found in the stock market at such a valuation is irresponsible.

Equity ratios on Wall Street houses are very low, as Citibank, and could be very vulnerable to a stock market crash. For example, Salomon Inc. had equity of 4.143 billion against 183.725 billion in liabilities, or 2.255% (See 1995 Annual Report). Therefore, the notion that the system must explode into a hyperinflation, as in Germany, has not the certainty some think. It could easily implode in a cross-default bank crisis where such defaults destroy massive amounts of bank credit, as in the deflation crises in Germany and the United States in 1929-33. It is the over-extension of credit and currency discussed in this paper which makes the system vulnerable to inflation and deflation crises.

15 Those, and the truly liberal Lafitte,

Are the true lords of Europe. Every loan

Is not a merely speculative hit,

But seats a nation or upsets a throne

Republics also get involved a bit.

(Don Juan, Lord Byron, page 41).

16 Source: Story related by Dr. Franz Pick when near death to a relative.

17 The Rothschild correspondent banker, J. P. Morgan and Co., made most of these Central Bank open market committee selections per Dr. Pick.

18 See Werner Sombart, The Jews and Modem Capitalism, translated by M. Epstein, Translation Books, New Brunswick, USA 1951, pages 104 and 105 describe Rothschild’s paramount importance in Europe.

19 This explains John D. Rockefeller famous exclamation that he couldn’t believe J. P. Morgan had so little when he died in 1913.

20 A Monetary History of The U.S., 1867-1960, by Milton Friedman and Anna Jacobson Schwartz, published by Princeton University Press, Princeton, NJ, 1963, pp. 407-419.

21 The net interest figure is found in the Federal Deposit Insurance Corporation Quarterly Banking Profile, 4th Quarter, 1996. It does not include credit union lending. This is the core statistic, as only these depositories can create credit through fractional reserve banking, and this checking account credit is used as currency, whereas other financial market debt as IBM, GM or Treasury bonds are not currency.

22 Ibid., D-4 — Table 1:9, and D-6 — Table 2.1.

23 Technology has a primary justification for military defense but could be handled as part of international negotiations to eliminate arms and its technology sources. That is, we must also disarm technologically and recycle the population back to the cities.

24 Life With Usury by Peter Jon Simpson, 30th Judicial District, Route 3, Box 324, Seymour, Missouri.

25 Ex. 22:25, Lev. 25:36,37, Deut. 23:19, Prov. 22:7.

26 For any usury country to return to an interest free system, using the USA status as example: (1) Immediate elimination of interest rates; (2) Debt repaid over a 7-yr period; (3) All debt released after that 7 years and at end of every 7th year thereafter; (4) Reserve requirements on depositories gradually raised to 100%, eliminating fractional reserve banking of 4 trillion in depository credit, while printing paper money to buy in the 5 trillion federal debt.

If we went to the 5 trillion figure in paper money we would wipe out the federal debt. If we then divided the 5 trillion in paper money by about 250 million ounces of gold at the Fort Knox depository, we would have for each ounce of gold a $20,000 per ounce value – gold backing of $20,000 for each one ounce available, on demand, at the Treasury.

The resultant economy would be truly free. National sovereignty would not be subordinated to a Bank for International Settlements Committee or to the Federal Reserve Open Market Committee regulating (manipulating) credit flows. This footnote is but a very brief procedural outline of rationale for a usury alternative.

However, the greedy international banking system will not voluntarily let go of their fraudulent system. An international economic collapse of their system will automatically divest them of control. That will be the time for countries to turn to the non-usury system herein outlined and supported by the foregoing documented analysis.

David Lifschultz

No comments:

Post a Comment